A Faster, More Reliable Banking Experience is Here!

February 8, 2025

Celebrating the 2025 Service Award Recipients: Investing in Our Communities

May 30, 2025

How to Calculate Home Equity

Determining how much equity you have in your home is straightforward:

- Find Your Home’s Current Market Value – This can be estimated based on recent sales of similar homes in your neighborhood. For a precise valuation, consider getting a professional home appraisal.

- Subtract Your Mortgage Balance – Check your most recent mortgage statement to see how much you still owe.

- Your Equity – This is the difference between your home’s value and your mortgage balance—the amount of your home you truly own.

For example:

Home value: $350,000

Mortgage balance: $200,000

Home equity: $150,000

Importance of Home Equity in Financing

Home equity isn’t just a number—it’s a powerful financial tool that can help you secure funds for various needs.

- Access to Affordable Loans – Home equity loans and HELOCs typically offer lower interest rates than credit cards or personal loans.

- Flexible Use of Funds – You can use your home equity for major expenses like home renovations, education, or consolidating high-interest debt.

- A Financial Safety Net – In times of unexpected financial strain, tapping into home equity can provide peace of mind.

Types of Home Equity Loans

The two primary ways to tap into your home’s equity are through a Home Equity Line of Credit (HELOC) or a Home Equity Loan (often called a second mortgage). Each offers unique benefits depending on your financial needs and repayment preferences.

Home Equity Line of Credit (HELOC): A Flexible Way to Borrow

A HELOC works like a credit card, allowing you to borrow against your home’s equity as needed, up to a set limit. It’s a flexible financing option that can help you manage ongoing or unpredictable expenses without committing to a large loan all at once.

- Access funds as needed – Instead of receiving a lump sum, you withdraw only what you need when you need it.

- Interest-only payments available – During the draw period (typically 10 years), you may have the option to make lower, interest-only payments.

- Lower rates than unsecured loans – HELOCs usually offer significantly lower rates than credit cards and personal loans, helping you save on interest.

- No need to refinance – You can access your equity while keeping your existing mortgage intact.

Home Equity Loan (Second Mortgage): A Lump Sum for Major Expenses

A home equity loan provides a fixed amount of money upfront, with a structured repayment plan and a fixed interest rate. It’s ideal for homeowners who need a predictable monthly payment and a set loan term.

- Receive a lump sum – Get the full loan amount at once, making it a great option for one-time expenses like major renovations or debt consolidation.

- Fixed interest rate – Unlike a HELOC, which typically has a variable rate, a home equity loan locks in your interest rate, ensuring steady payments.

- Substantial borrowing power – Depending on your lender and credit profile, you may be able to borrow up to 80% of your home’s value.

- Ideal for structured repayment – If you prefer a set schedule with a clear payoff date, a home equity loan offers stability.

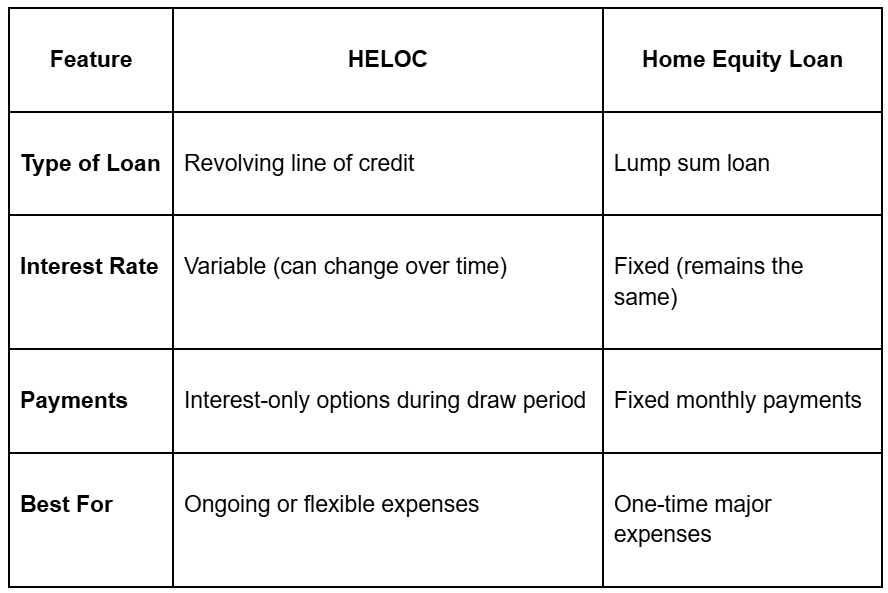

Key Differences Between a HELOC and a Home Equity Loan

While both options let you tap into your home’s value, they work differently:

Benefits of Home Equity Loans

Using the equity in your home isn’t just a way to access extra cash—it’s one of the smartest ways to secure low-cost financing for major expenses. Whether you choose a Home Equity Line of Credit (HELOC) or a home equity loan, both options offer lower interest rates, flexible repayment terms, and potential tax advantages that make them a more cost-effective alternative to credit cards and personal loans.

Lower Interest Rates Compared to Other Loans

One of the biggest advantages of tapping into your home’s equity is the lower interest rates compared to unsecured borrowing options.

- Save money over time – HELOCs and home equity loans often have much lower interest rates than credit cards and personal loans, making them a cheaper way to finance large expenses.

- A smarter way to consolidate debt – If you’re paying high interest on multiple credit cards, a home equity loan or HELOC can roll those balances into one lower monthly payment, reducing overall interest costs.

- More affordable home improvements – Instead of using a high-interest personal loan for renovations, you can borrow against your equity at a lower rate to upgrade your home without overspending on interest.

Flexible Terms and Repayment Options

A HELOC puts you in control of when and how you access your funds—making it one of the most flexible borrowing options available.

- Borrow only what you need – Unlike a traditional loan, a HELOC allows you to draw funds as needed rather than receiving a lump sum all at once.

- Multiple access options – You can access your HELOC funds through debit cards, checks, or online transfers, making it easy to use when you need it.

- Interest-only payment options – Some lenders, like Beehive Federal Credit Union, offer interest-only payments during the draw period, helping to keep monthly payments low while you manage expenses.

Possible Tax Deduction on Interest Paid

In some cases, you may be able to deduct the interest paid on your HELOC or home equity loan, making it an even more cost-effective borrowing option.

- Tax benefits for home improvements – If you use your HELOC or home equity loan to "buy, build, or substantially improve" your home, the IRS allows you to deduct the interest on your tax return.

- Maximize your tax savings – Unlike personal loans or credit card interest (which aren’t deductible), a home equity loan used for home upgrades could reduce your taxable income.

- Check eligibility with a tax professional – Always consult a tax professional to determine whether your use of home equity funds qualifies for deductions under current IRS guidelines.

Using Home Equity Loans for Financial Goals

Your home’s equity isn’t just a number—it’s a powerful financial tool that can help you achieve major financial goals while keeping borrowing costs low. Whether you’re looking to consolidate debt, finance home improvements, or cover unexpected expenses, a Home Equity Line of Credit (HELOC) or home equity loan can provide the affordable and flexible funding you need.

Consolidating High-Interest Debt with a Home Equity Loan

If you’re struggling with high-interest debt, a home equity loan or HELOC can be a smarter, more affordable way to regain control of your finances.

- Lower your interest rate – Credit cards and personal loans often come with double-digit interest rates, while home equity loans typically offer significantly lower rates.

- Streamline your payments – Instead of juggling multiple credit card balances, you can consolidate them into one manageable monthly payment at a lower rate.

- Improve your financial outlook – By reducing interest costs and making steady payments, you can pay down debt faster and save money over time.

Financing Home Improvements or Repairs with a Home Equity Line

Home renovations are one of the most popular and strategic uses of home equity, allowing you to increase your home’s value while improving your living space.

- Upgrade your home affordably – Whether you’re remodeling a kitchen, adding a new bathroom, or expanding your living space, a HELOC provides a cost-effective way to finance renovations.

- Flexibility for unpredictable costs – With a HELOC, you can withdraw funds as needed, ensuring that you only borrow what you use and avoid overborrowing.

- Enhance your investment – Many home improvements increase property value, helping you build even more equity over time.

Emergency Funding or Major Purchases with a Home Equity Loan

Life is unpredictable, and having access to your home’s equity can provide peace of mind when unexpected expenses arise.

- Cover emergency expenses – Whether it’s a roof replacement, major medical bill, or urgent car repair, tapping into your home equity can help you handle financial surprises without resorting to high-interest loans.

- Fund major purchases wisely – Instead of taking out high-interest financing, you can use a low-interest home equity loan to make large purchases more affordable.

- Pursue new opportunities – Whether you're launching a business or exploring an investment, a HELOC gives you access to low-cost, flexible funding.

Unlock Your Home’s Potential with Beehive

Your home equity is more than just a number—it’s an opportunity. Whether you want to consolidate debt, renovate your home, or prepare for the unexpected, at Beehive Federal Credit Union, we offer flexible home equity solutions with competitive rates, no annual fees, and reduced fees if your loan remains open for 24 months or more.

With low interest rates, flexible repayment options, and no annual fees, Beehive makes it easy to tap into your equity while keeping borrowing costs low. Plus, if you keep your loan open for at least 24 months, you’ll enjoy reduced fees, making it even more cost-effective.

Ready to put your home’s equity to work? Contact Beehive today to learn more about how a HELOC or home equity loan can help you achieve your financial goals—on your terms.

{kind=link}

{kind=link}

{kind=link}